Compensation in the life insurance industry incentivizes professionals to do things that are not good for clients.

If you remember this simple rule of thumb, you will be better-equipped to avoid expensive mistakes:

Start by assuming that compensation to the company or person you work with is correlated with the premiums that you pay.

Commissions or fees paid for the sale of insurance products tend to be 'front-loaded,' meaning agents earn a large percentage of their total compensation right away. This creates little incentive to ensure that clients will be willing and able to stay in their policies for the long term

Are there exceptions to those rules and variations around them? Sure. But directionally, that is the key point.

You can start to see the incentives created already:

- Incentive to sell permanent life insurance with more features and complexity ("fancier" product => higher premiums => higher compensation)

- Incentive to explain away bad underwriting outcomes, rather than advocate for the client (worse pricing for the client => higher compensation)

- Incentive to push inappropriately high amounts of coverage (higher coverage amount => higher premiums => higher compensation)

Scary - hence my decision to write about this on Halloween!

While I believe that not paying employees commissions is a step in the right direction, even when that's the case, the employer (i.e. the business itself) is still getting paid commissions. That's true here at AboveBoard and other brokerage agencies that have moved to this model (particularly tech-enabled ones).

Read very closely if you think a business selling insurance is "fee only" or "no-commission", and understand how they actually make money. The reality is that whether someone is paid based on "fees" or "commissions" or some other word for "money", money is money and any business has conflicts of interest -- the key issue is how those conflicts are managed, and how they are disclosed and explained to clients.

We often have clients come to us with policies they bought elsewhere before coming to AboveBoard, and many times those policies illustrate the repercussions of bad incentives. Building a better way was a key reason we started AboveBoard Insurance Services (AboveBoard Financial's independent life, disability and long-term care insurance brokerage).

A Real-Life Example of Bad Incentives Producing Bad Results

Speaking of seeing the fallout:

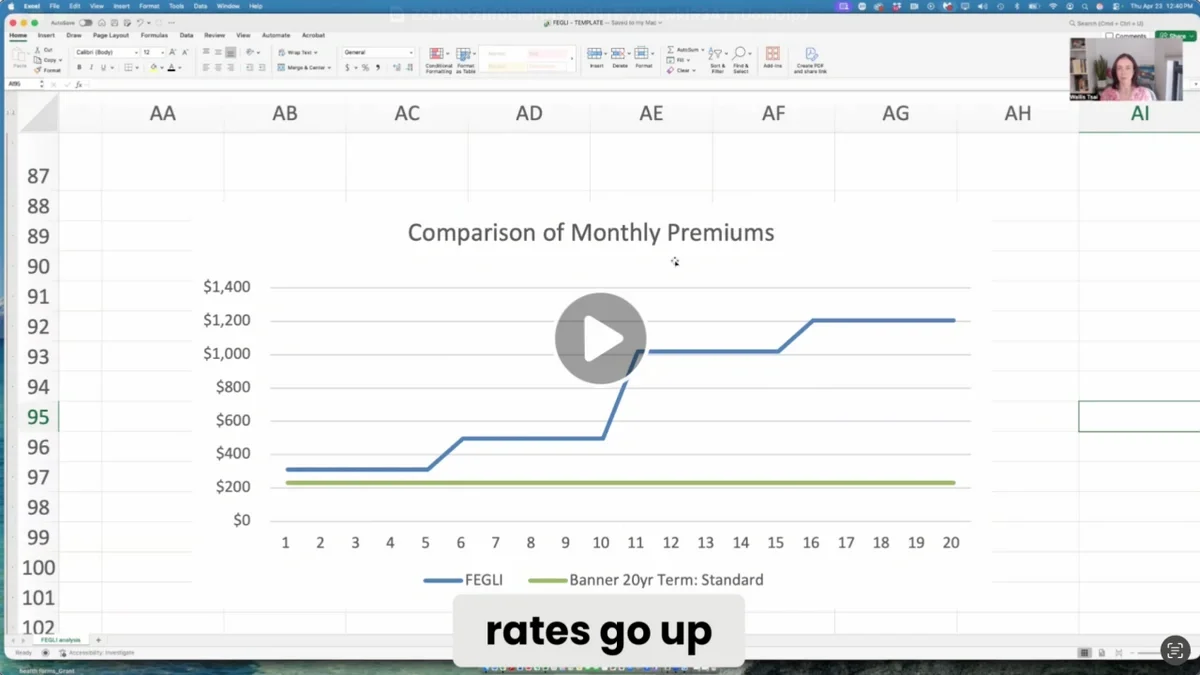

"Jackie", a doctor and mom of young kids, age 36 and in excellent health, had been sold a $1 million permanent policy with annual premiums of over $22,000 / year by a well-known, national insurance and wealth management company.

$1 million was a dangerously inadequate amount of coverage - if Jackie died prematurely, her surviving husband and children would have been massively short-changed.

The product was also totally inappropriate for her phase in life, as her money should have been focused on student loan pay down and her excellent workplace retirement plan (she wasn't even capturing the full match!).

Five years into this "insurance trainwreck" and knowing something was not right, she came to AboveBoard for help.

$3 million of coverage for 20 years was what she really needed, given her high income and important role caring for her children. And she could get it for only $2,005 / year - that's 3x the coverage for less than one-tenth the cost.

Term insurance and permanent insurance are not the same -- term insurance is a good choice for hedging the risk of premature death, whereas permanent insurance (e.g. whole life, variable life, universal life, etc.) is designed to pay a death benefit whenever you die.

But what Jackie needed most, as her top priority, was enough coverage to ensure her husband and kids would be OK if she died prematurely.

The right "next question" was whether her "additional available dollars" would likely earn the best return in permanent insurance, or other investments Jackie could choose. AboveBoard's recommended strategy allowed her to plough the difference in premiums (~$20,000 / year) into her workplace retirement fund, max out the match, max out low-fee, tax-deferred savings and still have something left over for getting tax-free growth in 529 plans for her children. The value of those actions would likely far exceed the value of the permanent life insurance.

Is Jackie someone for whom permanent insurance might make sense in the future? Absolutely. She is a highly compensated professional in a high tax bracket, living in a state with high tax rates. But it was not the right time when we met her, and it had definitely not been the right time 5 years earlier.

Her term policy includes an outstanding conversion option, allowing her to keep the option for her future self to buy permanent coverage at best pricing rates, regardless of future health. A perfect balance of today's budget constraints with her future self's potential goals and opportunities.

So why didn't she get good advice when she tried the first time, 5 years ago? Remember the rule of thumb. With the inappropriate permanent policy, the payout to the insurance agent was higher with the bad advice.

In Search of A Better Way

When we set up AboveBoard Insurance Services (AboveBoard Financial's independent life and disability insurance brokerage agency), I asked myself, "how do we build an ethical insurance brokerage agency that places clients' interests first and achieves the best outcomes for clients?"

We considered fee-based and low-load insurance models, and determined that those were not good paths for a few reasons:

- So few carriers operate that way that doing that would cut off access to most of the products in the industry, which has the perverse effect of making the consumer worse off most of the time.

- Fuzzy math - you have to be careful about a popular "shell game" in financial services: moving things around a bit and claiming it's something new and better. Charging someone "only" 75% instead of 100% but for...3 times as many years is different, but not better; it's actually worse.

- Doesn't really even make sense - When you buy a car, what you care about is the best price for the car you want. You don't care about how the manufacturer splits your money with the dealership, or what they call those payments. Similar deal with life insurance.

The life insurance industry is very old - it's one of the few sectors where it's common to see companies that are largely intact after more than 100 years. Things have been done a certain way for a long time. The life insurance industry is also quite good at doing a lot of things, such as pricing and managing risk. The products, when used appropriately, can be very useful and genuinely help people.

So how could we focus on the good, and appropriately manage the bad incentives that exist? The fact there's an incentive to do something does not mean you have to do it.

I ultimately concluded the right approach was to:

- Be radically transparent with consumers about how the industry works - hence these unusually direct blog posts (which you might not be surprised to learn are "frowned upon" in some circles!)

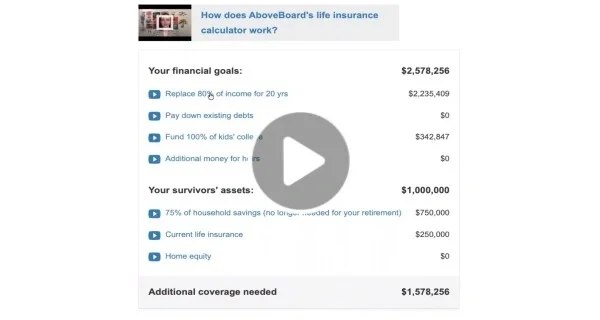

- Be radically transparent about how we reach our recommendations - hence our interactive life insurance calculator and willingness to talk through the results and personalize them based on our listening to your goals

- Build our process to be exactly what a savvy client would want done for them

- Publish AboveBoard Client Stories, anonymized real stories of what a consumer-first process looks like and how it helps people

- Apply rigorous analysis when considering permanent life insurance (e.g. whole life, universal life, variable life) and run the math to make sure that the life insurance truly provides a meaningful benefit to the client. To learn more about our approach, check out this podcast

To get a coverage recommendation and online quotes, visit our interactive life insurance calculator.

If you feel that you, like the person in our example above, might be stuck in a bad life insurance policy, email us at concierge@aboveboardfinancial.com for help.