Everyone wants to get the best deal on life insurance, but a lot of people have incorrect ideas about how to do it, or they just have not had time to figure it out yet. This post does that research for you.

When you go to buy a car, you know that the exact same car can cost different amounts, depending on who you buy it from. You also know that you can negotiate the price of the car.

Life insurance is the opposite - you cannot negotiate the price of any particular policy, and any particular policy will cost the same, regardless of who you buy it from. As a matter of law.

Even still, there are several important things you can do to save a lot of money on life insurance, and set yourself up well for the future:

- Get yourself matched with the right carrier for your unique profile

- Know what you need and what you don't need

- Manage your application process proactively to get assigned to the best tier possible, which means better pricing for you

- Be smart about your coverage, including choices around backdating, laddering & conversion options (don't worry if you don't know what those are, we'll explain shortly)

At AboveBoard Insurance Services, we take care of all these things for all of our clients!

To understand what you need to do and why, it helps to understand how the life insurance industry works.

A Quick Overview Of How Life Insurance Pricing Works

When you apply for life insurance, the insurance company assigns you a rating, which you can think of as a pricing tier. Which tier you get assigned to depends on on your health and lifestyle profile. Your goal (and our goal, when you work with AboveBoard) is to get you assigned to the best-priced tier for the life insurance product you want. (More info is in How Life Insurance Pricing Works.)

Insurance companies (aka "carriers") have really different ideas about who should qualify for different tiers. One carrier will say "4th-best tier" while another will say "best tier" for the exact same person.

Carriers have some fixed rules, but there's also a lot of judgment by the insurance carrier. How well your brokerage agency advocates for you can save you a lot of money.

You do not want a broker that just says "sorry, you pay more" and moves on to the next thing.

Figuring out which carrier will ultimately offer the best option for your unique profile is a key determinant, and great reason to work with a truly independent brokerage agency (like AboveBoard).

1) Get yourself matched with the right carrier for your unique profile

Different carriers often have very different ideas about how to price the same person.

For example, some carriers are comfortable offering best pricing to someone with depression & anxiety that's well-controlled on meds. Other carriers would never consider best pricing for that same person. Relatively minor events, like having a few moles removed, getting a few speeding tickets, or having mild gestational diabetes for a couple months before delivery can all drive big differences between carriers, too.

We track carriers' requirements and underwriting results, so we can guide you to the carrier that's most likely to extend you the best offer for life insurance coverage.

2) Know what you need and what you don't need

The biggest problems with life insurance happen when people have too little or too much.

"Too much" is when you've been sold permanent insurance inappropriately (that happens a lot), or the coverage amount is just much higher than what your loved ones would actually need.

"Too little" is relying on the 1x your salary coverage you have through work when you have a spouse and/or kid(s) depending on your income. Or when you got $1m 20 yr term before having your first, and 7 years later you just had your 3rd and your income is 50% higher.

Clear understanding of your life insurance coverage needs and your other financial priorities is the best way to get what you need and nothing you don't. That's why AboveBoard offers:

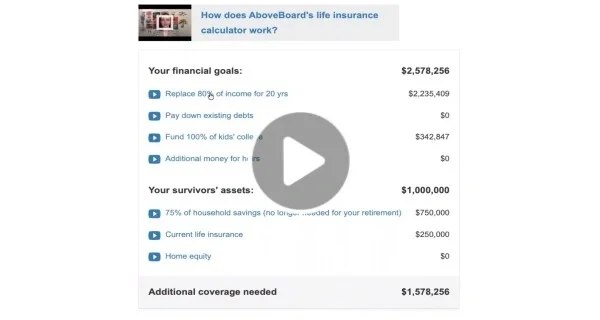

i) Our interactive, transparent life insurance calculator - you can easily adjust the assumptions if you wish, or ping us on chat or set up call and we'll walk you through how to figure out what you really need

ii) Our Financial Action Plan - helps you put your different financial priorities and choices in order; life insurance is only one piece of the puzzle

3) Manage your application process proactively to get assigned to the best "tier" possible

There's a lot that goes on behind the scenes at insurance companies. Underwriters (the people assigning you to a particular tier for pricing) are people, too. They appreciate clear, helpful communication. They're sifting through a boatload of information about you, some of which may have inaccuracies, or be unclear in a way that can be easily misunderstood or overlooked. Occasionally, they might make a mistake.

Prior the application, framing a client's "whole picture" is sometimes helpful. Perhaps a youthful indiscretion needs to be put in context or a higher-BMI person's healthy habits need to be highlighted to receive appropriate credit, and get assigned to a better tier. At AboveBoard, we tirelessly advocate for you - you can see some examples in our Client Stories.

Sometimes the insurance company's underwriting process turns up things that a client either didn't know about or forgot to mention. Or the medical records have inaccuracy, or the underwriter misunderstands them. When that happens, you want a brokerage agency that puts your best interests first, asks the right questions, and then hunts down answers:

- Is this a misunderstanding, and - if so - what can be done to correct it?

- Is this new information, and - if so - are there any better options out there?

At AboveBoard, we're constantly advocating for our clients.

4) Be smart about your coverage, including choices around backdating, laddering & conversion options

Even with the simpler insurance products - like term insurance - there are several levers you can pull to get a better deal for yourself. Don't worry if reading through these items doesn't feel fun - we think these details are super-interesting, and we take care of this analysis and advise you.

Backdating - insurance pricing is based on your age. You can choose to start your coverage a few weeks or months early, in order to get the less expensive pricing you would have gotten if you'd applied when you were just a bit younger. You cannot go back more than 6 months, so this may or may not be available to you, depending on when you apply. Even when it is available, the savings may or may not justify doing so. To make things just a bit more complicated, some carriers price you off your half birthday, others your actual birthday. Not to worry, we monitor this for you.

Laddering - setting up your insurance coverage as 2 or more policies that last different amounts of time (say a 20 year term + 30 yr term, or a mix of term and permanent) is called "laddering". Sometimes laddering makes sense, sometimes it does not. It's often not worth it (or can even cost more, definitely not the goal!) if you're under 40, able to get into a well-priced tier, or think that your income will increase meaningfully with professional advancement. But sometimes it's a great way to meet budget goals and not pay for what you don't need.

Conversion options - a conversion option is the right to convert your term coverage to permanent coverage at some point in the future, without having to prove you are healthy at that future date. Some conversion options are really good, others are not. You can often upgrade from "not good" to "really good" for anywhere from $0 to a few dollars more than your least expensive option.

Maybe you value that or maybe you don't, but it's a choice worth considering. Example of when it would be useful to "Future You": say you survive cancer in your 50s and wish the 20 year term you bought when you were 100% healthy in your 30s (and got best pricing) would last longer. With a good conversion option, you can get a policy that lasts the rest of your life at best pricing rates, even though you just got a clear scan after completing cancer treatment.

Ready to get a personalized quote from AboveBoard? Visit our interactive life insurance guide to compare quotes from 20+ highly rated insurance carriers.