Not all retirement plans are created equal. The variation in quality between plans can be huge.

At AboveBoard we’re fans of simple, clear language, especially when it summarizes complex analysis. Because of that, we’re not afraid to call out retirement plans that fall short as “crappy”

If you're lucky enough to have a match from your employer, then contributing enough to max out the match makes sense, even if the plan is otherwise less than stellar.

The question of whether an employer-sponsored retirement plan is the best place for your money comes up on the unmatched portion.

How to Tell If Your Workplace Retirement Plan is Good—401(k), 403(b), 457(b), etc.

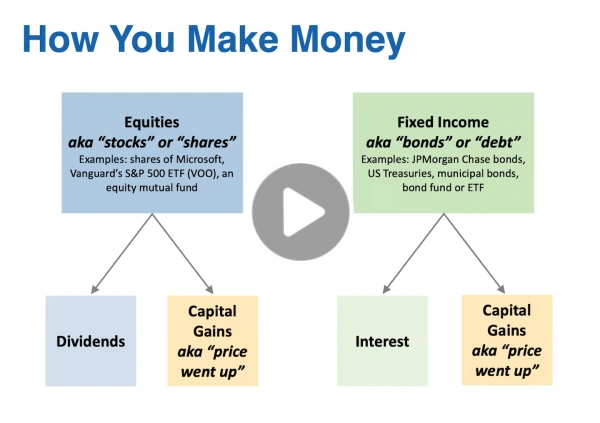

A good plan offers a range of low-cost investment options. It should include a solid selection of low-cost index funds. Having reasonably-priced, actively-managed funds on offer in addition to a robust offering of index funds is nice to have, but it's not essential.

The information about the investment choices that your plan provides should make it easy to assess performance of the different investments after fees. A table that compares the funds to a relevant benchmark is best.

Good plans do exist, but unfortunately some employer-sponsored retirement plans are not so good.

What Makes a Crappy Retirement Plan?

One marker of a crappy retirement plan is fees that are higher than the market rate. Looking at expense ratios can tell you how your plan measures up.

Here's how to check: look for whether you can buy a low-cost US equity index fund (e.g. "S&P 500" or "US Total Market Index") with an expense ratio of 0.30% or less. If you can, great! You do not have a crappy plan. To be clear, this is not a tall order. Vanguard charges retail investors 0.03% for its Vanguard 500 ETF, so 0.30% is a very generous threshold to aim for.

If you can’t find that, look for a "US large capitalization stock" mutual fund or ETF, meaning the fund owns stock in large US companies (think Apple, Verizon, Exxon, etc.). If the expense ratio is <0.50%, then it's probably worth it for you to contribute.

If the expense ratio is 0.50% or higher, it’s increasingly likely you have a crappy workplace plan. The fees on your workplace retirement plan are meaningfully above the market rates, which is something your employer can and should fix.

So You Have A Crappy Plan…What Now?

Having a crappy retirement plan is disappointing. Now you have to ask yourself if it still makes sense to contribute.

Before you decide if you still want to contribute to the unmatched portion of your retirement plan (versus saving your money in an IRA and,if you can contribute more than the annual IRA limit, a brokerage account), ask yourself these questions:

-

Are you eligible to contribute to a Roth IRA?

If so, a Roth IRA (where you can control the investment choices) might be a more attractive option than the unmatched portion of your workplace retirement plan. If not, the analysis is a bit more complex, but the odds are good you'll still want to contribute to your crappy workplace retirement plan. -

What are the odds you’ll still be working at your current employer in 5 years? 10 years?

If you think it’s unlikely you’ll stick around for more than 5 or even 10 years, go ahead and make the contributions, knowing that you can roll over that crappy workplace plan into either an IRA or your new employer’s hopefully-not-crappy plan when you change employers. -

Does your plan allow in-service rollovers?

You need to understand the details of your employer's plan. Some plans allow you to rollover even when you're still working there, so if you can get the tax-advantaged contribution and not be with the bad plan for very long, that can be a great option. -

Are you in a position to effect a change in the crappy plan?

Your employer could offer something different and better. Only you can assess if it’s feasible and worth your “political capital” at work to try to effect this change. -

What are the odds you'll apply for financial aid for your kids/future kids?

Financial aid calculations exclude retirement accounts, so if you think there’s a good chance your family will apply for financial aid, getting as many assets as possible into a retirement plan (even a "crappy" one) is generally a good idea.

It might still make sense to make an unmatched contribution to your workplace retirement plan even if it is "crappy," but you should also consider the other options available to you. Our free Financial Action Plan can help you think through your options.