Getting the right amount of term life insurance involves staying connected with a healthy balance of fear and faith -- fear that things could wrong, balanced by faith that you are very likely to outlive your term policy.

Smart Personal Risk Management: A Case Study

Let’s start with a case study about Lindsay* and Terrence*. Terrence is a physician and Lindsay was on hiatus from Broadway shows during the COVID-19 pandemic. They have 3 young children. They came to us seeking $10 million of coverage for Terrence, which would represent about 20 times his annual income.

This is a tale of reasonable concerns and bad advice. Lindsay was very worried about the family losing Terrence’s income if he died (totally reasonable), and another insurance agency had told her that $10 million of coverage was the right amount (bad advice, given their specific life situation!). She became suspicious when the other agency pushed a permanent policy with over $70,000 in annual premiums (yikes!). Then she reached out to us.

During the initial conversation with Lindsay, we asked how our suggestions fit with the family’s budget, and she said, “we’ll pay whatever it takes to get coverage.” That is music to many insurance agencies’ ears, but not at AboveBoard. We want to help each of our clients practice smart personal risk management, and that starts with balancing different risks and priorities.

So, did this family really need $10 million of coverage? Lindsay completed our life insurance calculator and spoke with an agent, and we determined they did not need that much coverage, and instead $7 million was the right number. Additionally, she completed the Financial Action Plan, and we found that the $70,000/year in proposed whole life premium costs could be put to much better use by paying a fraction of that towards life insurance and putting most of it towards maxing out tax-advantaged retirement savings vehicles and 529 plans for the kids. There is no planet on which the policy with over $70,000 in annual premiums that the other agency promoted would make sense for this particular family!

That’s just one example of how our agents help customers look at the whole financial picture. Continue reading to learn how to better assess your financial situation and practice smart personal risk management.

*We never use real names, and always change any potentially identifiable information.

3 Simple Steps to Practice Smart Personal Risk Management

How do you identify a smart personal risk management strategy? Ask yourself these three questions:

- What is likely to happen? How do I plan for it?

- What could go wrong? How do I plan for that?

- How do I strike the right balance between one and two?

This framework works really well for many financial topics. Let’s talk about how it applies to purchasing life insurance.

1) Ask Yourself: What is likely to happen? How do I plan for it?

What is likely to happen?

Average life expectancy in the United States is 77.5 years.

If you are fortunate to be healthy and a non-smoker, then I have more good news for you: the odds are excellent you will live to a ripe old age, into your 80s or 90s at least.

Anytime you can qualify for a term life insurance policy, that is because the insurance company believes the odds are excellent that you will outlive it. You buy term life insurance to protect your loved ones in case you’re among the unlucky few who die prematurely.

In this step, we want to identify the “base case,” or the likely future outcome that we are planning for. For a healthy non-smoker the “base case” is that you will need money to fund a long retirement, and at some point in your later years you will reflect on your legacy, including what you want to pass on to the people and organizations you care about most. Life insurance is often an effective way to craft a strategy that achieves your desired result.

How do I plan for it?

Long life expectancy means you will likely need to fund your (long) retirement. Enjoying that time in the style you want requires savings.

We apply smart personal risk management to our advice. We don’t want you to buy too much coverage, because we want you to have room to save for the most likely scenario - that you live into retirement. We want you maxing out your 401k match - and maybe even the unmatched portion, depending on your tax situation - before you even seriously consider permanent life insurance.

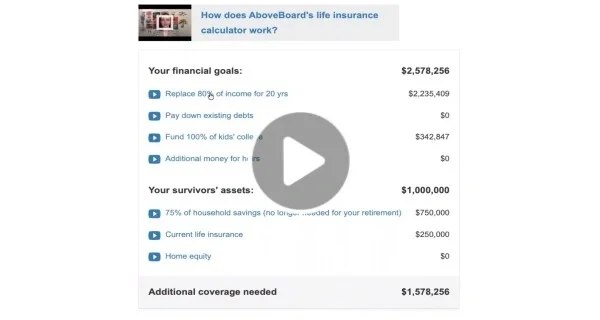

A smart strategy is to get the right amount of term life insurance coverage today, which means ensuring your family would be financially secure if you died prematurely. AboveBoard’s life insurance calculator helps you identify the right coverage amount for you. You can also learn more about how this analysis works here.

The best strategy also considers options you might want later in life, assuming you’re still a reasonably healthy person (the “base case”). Subtle differences in term policies can have a big effect on your options later in life. We recommend you consider getting a term policy that gives you the “conversion option” that best fits your situation and goals. A “conversion option” is the right to change your term coverage into lifelong permanent coverage without having to prove you are still healthy.

Not all conversion options are created equal. Different conversion options are best for different people and goals.

If you are on a solid financial trajectory, you may benefit most from a conversion option that sets you up to one day convert your term coverage into a lifelong permanent policy; these are popular among affluent families when doing retirement planning or estate planning.

If you feel like your financial situation is not on such solid footing, then you might reasonably choose the cheapest term coverage available, regardless of what conversion options it offers.

Both approaches are reasonable choices; smart personal risk management involves making an informed decision about what’s right for you.

2) Ask Yourself: What could go wrong? How do I plan for that?

What could go wrong?

The worst case scenario is that you die prematurely without adequate life insurance coverage, leaving loved ones who depend on your income or care struggling to fill the void. You can absolutely remove the financial burden with life insurance, which makes it much easier for loved ones to navigate the emotional toll of loss.

There are different degrees of “going wrong”. Dying while you have young children at home is generally more financially catastrophic than dying when they’re in college. Both situations are tragic, but the financial impact is different.

“Going wrong” doesn’t always mean premature death. It could mean receiving a serious diagnosis where your prognosis is pretty good, but still tenuous, leaving you wishing you’d chosen a longer term than what you have, just in case your prognosis doesn’t turn out well down the road.

Choosing the right term policy for you can address these risks.

How do I plan for it?

To address the risk of premature death, you need an amount of coverage and a term that would provide for your loved ones if you were gone. Advice that says “most people should have $1 million” or “get 10x your income” is usually wrong for specific individuals, so it’s really important to take into account the specifics of your financial situation and what choices you would want your loved ones to have if you died prematurely. Our life insurance calculator helps you do just that.

To address things that can “go wrong” towards the end of your term other than death, consider what conversion option is included in your term policy. How long does the option last? What does the coverage convert to? Conversion options are not all the same, so you’ll want to make this choice carefully.

If you’re worried about the risk of being sick at the end of your term but your budget is tight today, there are policies that do a good job of cost-effectively providing options for you in a downside scenario. Other term policies offer additional conversion option features that are better-suited for families who are already affluent and likely to engage in passing money to future generations down the road, or who have a very high tax rate.

We go into greater detail on conversion options in this post.

3) Ask Yourself: How do I strike the right balance between 1 & 2?

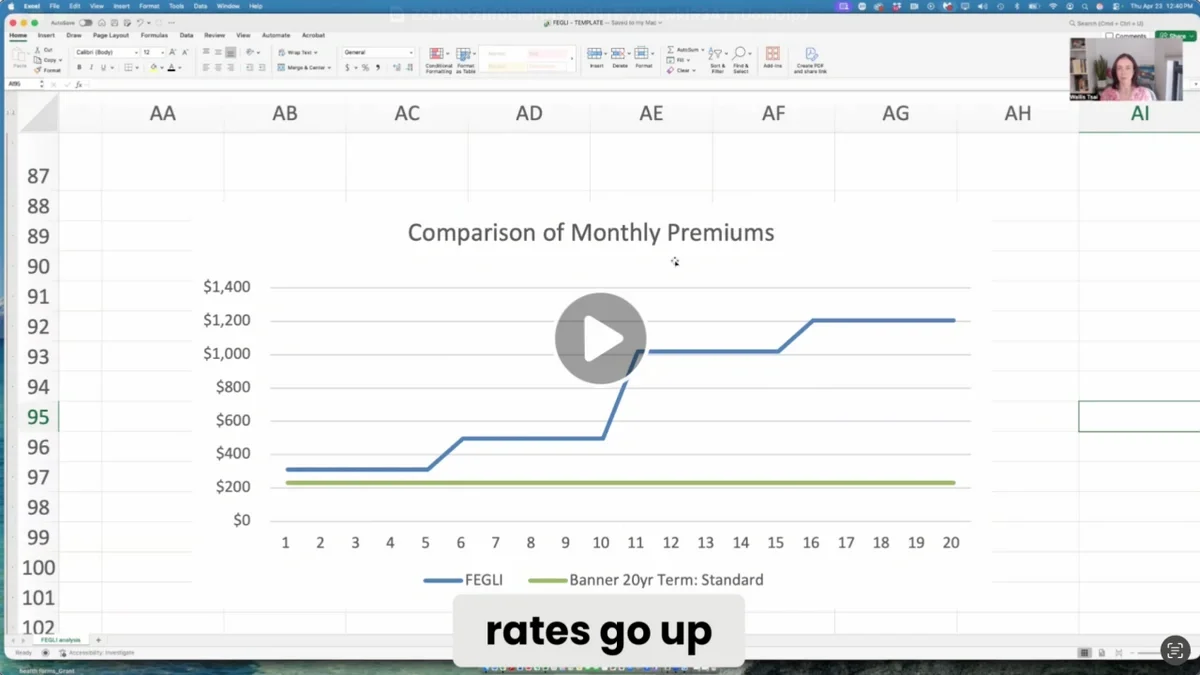

Striking the right balance of planning for what’s likely and planning for what can go wrong usually depends on knowing the pricing of the options you’re considering. There’s not one right answer for everyone. It's a question of the best balance for you. You might be surprised to learn how inexpensive life insurance is—our instant online quotes help you understand your options.

A common question we get from clients with young children is whether a 20 or 30 year term is best. The answer is that it depends on your goals. 20 year term coverage will usually take the worst case financial scenario off the table— that is, leaving young children and possibly a surviving parent without the resources they need to maintain their lives. However, 20 year term coverage will usually not cover a younger adult’s entire expected working life.

30 year term ensures that most (or all) of a younger adult’s working life is covered, which can help with supporting a surviving spouse’s retirement, or even creating the freedom to take early retirement if you’re diagnosed with a terminal illness at a time in life when you expect to be preparing for a long, happy retirement after a few more years of work.

Either term is a reasonable choice; it’s a question of which trade-offs are more appealing to you.

How To Get Started

The best place to start is to get a coverage recommendation with our life insurance calculator - it’s interactive and advice-focused, helping you map your goals to the best policies.

If you already know how much coverage you need, get an instant online quote.

You’ll have the opportunity to chat with or book a brief call with a life insurance expert who can look at your recommendations in real-time with you and help you practice smart personal risk management. Or, if you want to proceed directly to applying for coverage, you can do that, too.