Choosing the right term for life insurance is an important decision. Choosing the wrong term could mean adding financial distress to your loved ones’ grief at your passing. Today I’m sharing best practices for figuring out both what you need and what you may want for term life insurance.

Definitely check out our interactive life insurance guide, which will make suggestions for you based on the information you share about your situation and goals.

It’s important to get the term right upfront

It’s in everyone’s best interest for you to choose the right term for you at the time you are buying your policy. You can do this by making sure the term covers you for as long as you expect to have people depending on your income (or care that you provide for free).

Sometimes people have the idea that it’s easy to extend your policy at the end of your term at a price similar to what you were paying during the initial term, but that is incorrect.

Although you can extend your coverage beyond the initial term with most policies, it’s typically very expensive for the coverage you get—either the premiums go way up, or the death benefit goes way down. Neither is a good outcome for you if you want to continue your coverage at inexpensive term insurance rates.

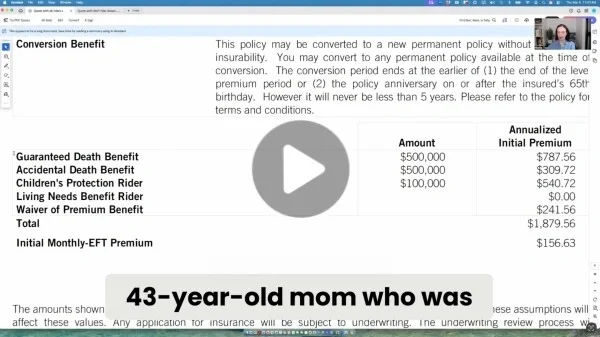

Also beware of assurances that all term policies can be converted to permanent life insurance. While often true, the menu of policies you can convert to can be very limited, including policies that are expensive for what you get and would make sense only if you were gravely ill at the time. While the ability to convert your term coverage to permanent coverage can be very valuable, the conversion option is not a good substitute for choosing the term you actually need. You can learn more about conversion options in The Option to Convert Your Term Life Insurance to Permanent - A Smart Move or Not Worth It?

How to choose the right life insurance term

The main question to ask yourself when deciding on the correct term for your needs is “how long will my dependents likely depend on my income or the care I provide?” Dependents most often refers to a spouse/partner or children, but can also include parents, siblings, or anyone else who counts on your income or the care you provide for free.

Your term options will generally be 10, 15, 20, or 30 year terms; some carriers offer 25 year term, a few offer 40 year term, and a handful offer other terms.

Consider your child(ren)’s age

You probably want to provide financial support to your child(ren) through college graduation. Here’s an example: Say you work outside the home, and your youngest child is 3 years old (no plans for additional kids). Your youngest will likely finish college in 18 years, so 20 year term would cover them through the end of college.

Consider your spouse or partner’s retirement plans

If you have a spouse or partner, it’s also important to ask yourself: “will that person likely need your income after your kids are financially independent?”

People often miss the fact that dual-income households can have "financially codependent" spouses who will need each other’s incomes to reach the retirements they want. If that financial codependency will likely last longer than the time the child(ren) are dependent, then a longer term might be needed.

For example: Following along on the previous scenario, you may feel confident that 20 year term will get all your kids through college, but when you think about saving for retirement, you worry that your spouse might not be able to comfortably retire if your income vanished the day after your 20 year term expired. In this case, 25 or 30 year term may be a better choice.

In other instances, two-parent families feel that their retirement savings are on track enough that, if one spouse died around the same time the kids become financially independent, the surviving spouse would be able to retire comfortably with the future nest egg and their own income.

Now you know how to think through choosing the right term. But there are also times when you can go for a shorter or longer term.

When it’s OK to buy a term shorter than how long you’ll have dependents

There are two common times when it’s reasonable to buy a shorter term than the amount of time you expect to have people who depend on your income or care.

1) When you can likely “self-insure” the last few years

Example: Say you just had twins. You feel your family is complete and don’t expect to have more children. You want to cover them until they are age 21 (21 years from now). Do you need 25 or even 30 year term? Not necessarily. You might be just fine rounding down to 20 year term.

To decide, you can ask yourself: If you have a spouse/partner, would they be able to comfortably retire on their own income plus your future nest egg if you passed away the day after the shorter term expired (in this example, that’s 20 years in the future)?

If your answer to that is that you feel you are on track with retirement savings and expect that in 20 years you’ll have enough saved to either comfortably cover retirement for one person or—with continued savings from the surviving person—they’d be able to fund a good solo retirement, then you can probably round down without undue risk to your family.

If your answer is that after putting two kids through college, you’d expect to need to really power up your retirement savings for several years to be on track for the retirement you want (even if only for one partner), then you should think about going longer than 20 years.

2) When the shorter term is already at the outer limits of what you can afford.

If you have dependents, something is always better than nothing. If you’d like coverage for 30 years, but 20 years is what you can afford, do not just sweep this matter under the rug.

Rounding down is always better than nothing.

Also consider whether you can reduce coverage and term to meet your budget goals. One of our insurance experts can help you find the trade-offs that best suit your goals, including your budget. Visit our insurance guide for more info, including how to easily contact a human expert for assistance.

When you should consider choosing a longer term

There are some situations where buying a longer term policy may make sense, when you can afford it.

1) If you think you might have more kids

If you think you might have more children in the future, choosing a longer term will give you the option of having inexpensive term coverage for longer. It’s sometimes difficult to know when your hope for additional children will come to fruition, but it’s almost always the case that the policy you buy now will be cheaper than the one you buy later.

2) When you hate the idea of dying and have the budget to afford a longer term than the minimum necessary term

Dying sucks, particularly when it happens before you’ve enjoyed a joyful old age. Whether it’s your kids’ (and grandkids’) lives that you’d wanted to live to see, time with a spouse, partner, and/or friends that you looked forward to, or places in the world you had hoped to explore, the idea of missing out is crushing.

If you’re diagnosed with a terminal illness, term life insurance can provide extra funds if you happen to receive bad news before you’ve had a chance to enjoy the retirement you want.

Some policies let you access a portion of the benefit early, while you’re still alive, if you have a terminal illness, or you might decide to spend more of your savings, knowing that your loved ones will receive your life insurance benefit.

This option is a “luxury good” of sorts—you do not need it, but you may decide you want it.

3) When you’re wealthy or on track to be wealthy to a degree that triggers estate tax

Permanent (not term) life insurance can be helpful with estate planning. Many high-earning people do not need permanent insurance today, but they might find that being able to get permanent insurance in the future—regardless of their health at that time—is very valuable for estate planning, because properly chosen permanent life insurance offers attractive returns and can optimize tax efficiency. (You can learn more about using life insurance for estate planning in Irrevocable Life Insurance Trusts and When does permanent life insurance make sense?)

You can guarantee yourself the option, without obligation, to convert your term policy to a permanent policy by buying a term policy with a good conversion option. Getting a longer term and a good conversion option gives you that option for longer.

We go into more detail about how people with higher levels of wealth and/or future earnings can benefit from a term policy with a good conversion option here.

Again, getting coverage for longer than you need is a choice, not a necessity. It can be a good choice for people when it’s a well-priced option, you can afford it, and one or more of these scenarios resonates with you.

Check out what term we recommend for you in our interactive life insurance guide. It will also help you understand if you’re in the group of people who should even consider permanent life insurance (spoiler alert: most people should stick with term).