*Written for Fellow Math & Finance Nerds (Anyone is Welcome!)

If you are ready to dive into the details of how we think about the correct way to calculate life insurance coverage amounts here at AboveBoard, then you are in the right place! Welcome, fellow nerds. (If you’re more interested in a quick explanation without the nitty gritty, then you might want to start with this overview instead.)

Our interactive Life Insurance Guide calculates a coverage amount for you using assumptions that are reasonable for many people, then empowers you to change those assumptions so you can tailor them to your situation and goals.

If you want an expert to guide you through it or just serve as your thought partner in this exercise, ping us on chat when you’re there!

Overview of Our Calculator

Let’s start with an overview of the key drivers for your life insurance coverage calculation. To be clear, this calculation focuses on situations where you want to replace the income you earn and / or care you provide for free for loved ones (vs. estate planning, business insurance, etc.).

(This will look familiar to you if you’ve read our quick overview, or used our calculator already.)

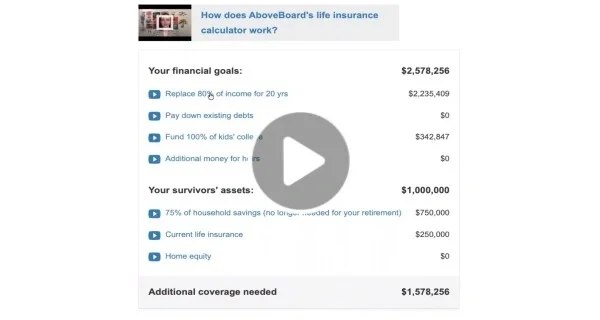

+ Income you’d replace for the number of years your loved ones need It

+ Debt you’d want your loved ones to pay off

+ Kids’ college (a contribution, not necessarily 100%)

+ Any additional inheritance you’d want to leave (0 is fine, too)

- A portion of your existing savings

- Life insurance you already have and want to keep

= Your life insurance coverage amount

Some things to keep in mind:

- Any surviving spouse will still need retirement savings.

- Sometimes you should replace your existing coverage, sometimes you should keep it. The right answer always comes down to whether you can improve on what you have in the market today. (We can run that analysis for you. Spoiler alert: most people can do better than any workplace coverage they might pay for individually, and you should assume the coverage your employer pays for would not follow you to your next job.)

The Starting Assumptions In Our Calculator

What Percentage of Your Income Should You Replace?

Our starting assumption: you’d want to replace 80% of your estimated after-tax* income.

*Tax rates can vary a lot by person - paying only Federal taxes in Miami is quite different from paying Federal, state & local taxes in NYC, where NY state plus NYC can easily run 10% or more. Our interactive Life Insurance Guide lets you tailor this to your situation.

Losing a grown-up from a household reduces household expenses, but often not by a lot. Most families don’t plan to move homes or radically change their standard of living if you or a spouse / partner died young.

Additionally, in a household with two adults, the surviving adult still needs to save for their own retirement, pay for health insurance, etc.

When it makes sense to replace a higher percentage of your income:

- You feel like you’re currently not saving very much money, or

- You are making life choices that assume future income increases

A “higher percentage” would usually be in the range of 85% - 100%. It usually does not make sense to go above 100%. (However, it can sometimes make sense to go over 100% if you expect a meaningful increase in income sometime soon.)

Example: you’ve enrolled your oldest in private K-12 (footnote: that’s $50k / year in NYC!) and expect to do the same for your 2nd & 3rd, given your escalating compensation scale at Investment Bank X.

Example: you and your spouse bought a home that’s a “reach” - you can manage today, but it will feel much better after your anticipated promotion next year.

When it makes sense to replace a lower percentage of your income:

- In any scenario where you’re gone too soon, your surviving loved ones would move to a much lower-cost-of-living situation than what you’re doing today (make sure you’ve clearly discussed this in advance will your loved ones, and everyone is on board!)

- You are saving a lot of money today, definitely more than what your surviving loved ones would need to be saving for their own needs, including their future retirement

Example: you and your spouse love New York, but if something happens to one of you anytime soon, you two agree the surviving parent & kids would be back home to Texas the next school year. The kids would attend the excellent public school with all the cousins. In this case, maybe you don’t need to replace 80%. But keep in mind you probably don’t want to be “forced” to move the kids anytime during 8th-12th grade.

How Long Should You Replace Income For?

You need to replace your income for as long as you expect to have dependents - people whose fundamental well-being depends on your income and / or care you provide for free.

Oftentimes, this is determined by how long you plan to support your children. Other times, it is a spouse whose comfortable retirement depends on your income. Occasionally, it is the expectation of caring for one’s own aging parents, or another loved one with special needs.

Example: you have a 3 year old and are expecting your second child. You feel your family will be complete with the two kids. You want to support them through college, possibly graduate school or young adulthood, say age 25. At a minimum, you should replace income for 21 years, but may also want to consider 25 years. (This is a different - but related - question from the right term, which we go into here.)

Should You Plan to Pay Down Debt with Your Life Insurance?

Our calculator assumes you pay down your debt if you die (alongside replacing 80% of your income, as described above). While some debt (like Federal student loans) are discharged upon death, most is not. Your mortgage payment won’t be discounted if someone dies.

Our thinking here is also driven by the fact that unexpected expenses crop up when a grown-up is gone early: therapy, flying in family members to try to “make up for” the absence, increased child care, and generally trying to reduce other sources of stress.

However, if you decide to replace 100% of your income, you might reasonably decide that replacing your income completely allows your loved ones to cover any debt payments.

What About College Savings?

This one depends on both your personal goals (private college at ~$70,000 / yr is different from in-state tuition at ~$30,000 / yr) and how much you’d be expected to pay for your kids’ higher education.

Our calculator assumes that you’d want to have a sizable contribution to your kids’ college savings fully funded if something happened to you – one less thing for your surviving family to worry about.

We make a rough estimate of what your family might be expected to contribute based on your income (side bar: the actual formulas used by universities - both FAFSA for Federal aid and the calculations that private schools run - are quite detailed; our calculator only uses a rough estimate). If you feel strongly that you want to stand ready to pay cash for 100% but our calculator didn’t assume this, you can easily make that change (ping us on chat if you need help).

However, if someone’s life insurance coverage is very expensive or they're simply trying to minimize budget, this is one of the first places we’ll say it’s OK to “shave down” your coverage amount, but we might also recommend boosting income replaced to 90% or 100%.

Replacing 90% or 100% of income often allows your loved ones to save for college what you would have saved anyway.

Do You Need to Leave Any Additional Inheritance?

No, you do not. Most people leave this at zero and that is fine. You can obviously choose something different if you’d like, but the important part is really getting right the other things we’ve already covered.

What About Existing Savings? Is It Possible to Have Too Much Insurance?

Yes, it is definitely possible to have too much insurance. We don’t want you to be over-insured either - that would be wasting your money.

If you have already saved a lot for your own retirement or your kids’ future education, we want to “count” that. Insurance does not need to cover that because you already have money on hand to cover it.

For families with two grown-ups, it’s important to keep in mind that comfortable retirement for one costs less than comfortable retirement for two, but probably more than half-price.

Additionally, many retirement savings accounts require that taxes be paid in the future when you withdraw the money, so assuming it’s all free-and-clear if someone dies would be incorrect (and lead you to think you have way more money available than you actually do).

Therefore, we assume that 25% of your existing household savings are available to offset the things you’d need to cover if you were gone (if you're married and filing jointly). If you're single, we 75%. (We recognize that marital status might not reflect the reality of your situation. If you feel like this assumption might not be right for you but are not sure what to choose, hit us up on chat when you’re at our interactive Life Insurance Guide, and an expert can help you adjust the calculation to your situation.)

Should You Count Your Existing Life Insurance?

It might make sense to try to replace your existing coverage, but only if you can truly improve on what you already have. And you should NEVER drop your existing life insurance coverage until you have formally accepted coverage from a new carrier.

The right strategy is always to apply for new coverage first, wait to see if you get what you applied for, formally accept new coverage when it comes through, and only then drop the old coverage. This avoids becoming accidentally uninsured, or ending up with something worse than what you had.

If your existing life insurance is through your workplace, then the odds are excellent that we can find a better deal for you, and therefore you should apply for enough life insurance that you’re effectively “not counting” your workplace coverage. We go into the details of how to think about workplace coverage - and whether you should replace it - in another post.

Last Bit of Advice

AboveBoard Insurance Services is an independent insurance brokerage. No, we do not think everyone should spend as much money as they can afford on insurance. The goal is accuracy. We’re here to help you get what you need, and nothing that you don’t!

Visit our interactive Life Insurance Guide for thoughtful, facts-based advice, and hit us up on chat with any questions.