The idea of skipping disability insurance and just "self-insuring" can sound appealing at first, especially if you’d rather invest the premiums yourself.

In this case study, we walk through that question using real quotes and a practical example based on the kinds of situations we often see. The goal is to help you see what self-insuring would actually mean for your savings if a disability happened, and why that approach usually does not work well unless you already have enough saved that you’d be comfortable retiring today.

Table of Contents

- 0:00 Overview of our agenda for this video

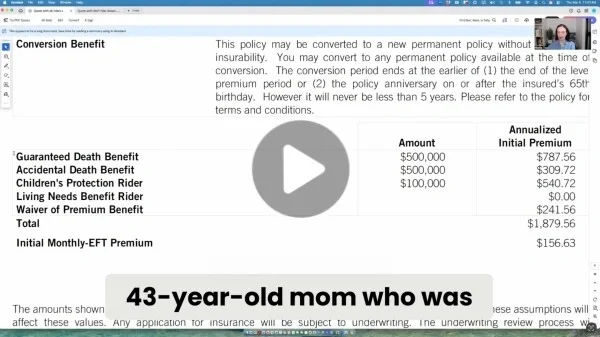

- 1:41 Looking at the two quotes being considered

- 7:07 How does what he could get from disability insurance compare to what he could get from investing the premiums? Let’s use Excel to find out.

- 16:15 What does the future look like if he experiences an "average"-length long-term disability of 3 years?

- 18:18 How to think about self-insurance of disability risk, and the "thinking trap" you should avoid

Video not loading? Click to watch on YouTube

To explore your options, you can begin by getting quotes for disability insurance.