People kept asking me what I thought of Gerber Life Child Life Insurance, aka the Gerber Grow-Up plan. The more I learned, the angrier I became. How could this trusted brand sell such an awful product?

I even took out a policy on my own 1 year old daughter, to see up close how it works. (There’s a 30 day free look period in New York state.)

What I found was so much worse than I ever imagined. I’m going to lay it out here, so you have the benefit of this information:

1) Gerber Grow-Up Plan cash value is a terrible investment

Gerber says: “Build cash value”

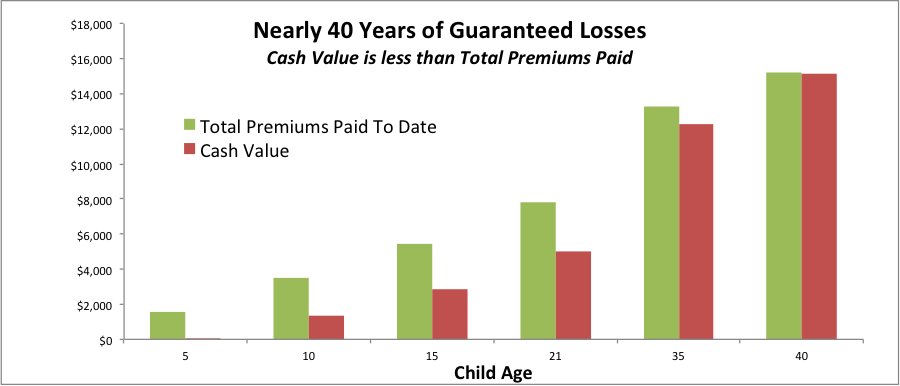

The truth is: Gerber’s guaranteed cash values would lock my daughter and me into a loss for nearly 40 years.

The green bar is how much I’d pay in premiums, the red bar is what we’d get back if we wanted the money for – as Gerber likes to advertise – “college textbooks” or a “down payment on a car”.

I could literally put cash in a mattress and come out with a better return (zero) – after nearly 4 decades of diligent savings – than with the Gerber Grow-Up Plan.

Gerber’s customer testimonials show a mom saying, “you put pennies in a change jar, put ‘em in a policy!” My heart breaks when I hear this. Pennies in a change jar would actually be a better investment than the Gerber Grow-Up Plan, at least for the first four decades.

2) Children and their families miss out on so much with a Gerber Grow-Up Plan

Gerber says: “Give your child a head start”

The truth is: there are many, much better ways to give your child a head start financially

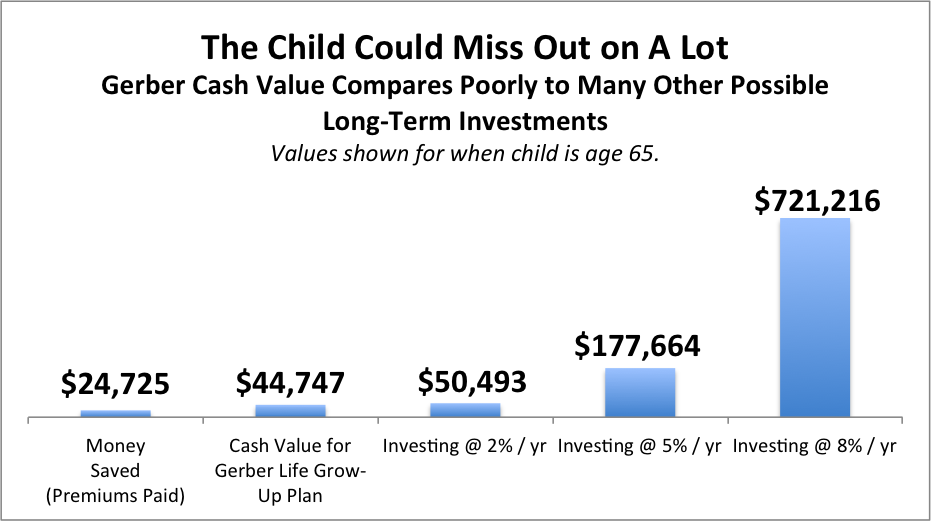

Warren Buffett rightly sings the praises of compound interest. Any child lucky enough to have a parent or grandparent ready to set aside money on their behalf has a tremendous opportunity: to enjoy the benefits of compound interest over a very long time.

Sadly, that opportunity is wasted with a Gerber Grow-Up Plan.

We saw above that my daughter would get back less than I paid in even after nearly 4 decades of diligently saving money.

You might wonder, does it get much better over time, when she’s much older? No, it does not:

After nearly 65 years of diligent savings, Gerber cash value would offer a tiny 1.7% annual return, unlikely to even keep up with inflation. Awful.

3) Gerber life insurance is really, really expensive insurance (part I)

Gerber says: “Coverage doubles at age 18 at no extra charge”

The truth is: Selling you a Ford Fiesta for $80k would be wrong. Selling you two Ford Fiestas for $80k is still really, really wrong. Same idea with Gerber – doubling what you get at "no extra charge" is still a bad deal.

General life experience in the USA conditions us to know that $80k – or even $40k – for a Ford Fiesta is ridiculous. (No disrespect to the Ford Fiesta, my family had one growing up, perfectly pleasant car -- but definitely not a $40k one!)

General life experience does not really equip us to know whether life insurance premiums are a good deal.

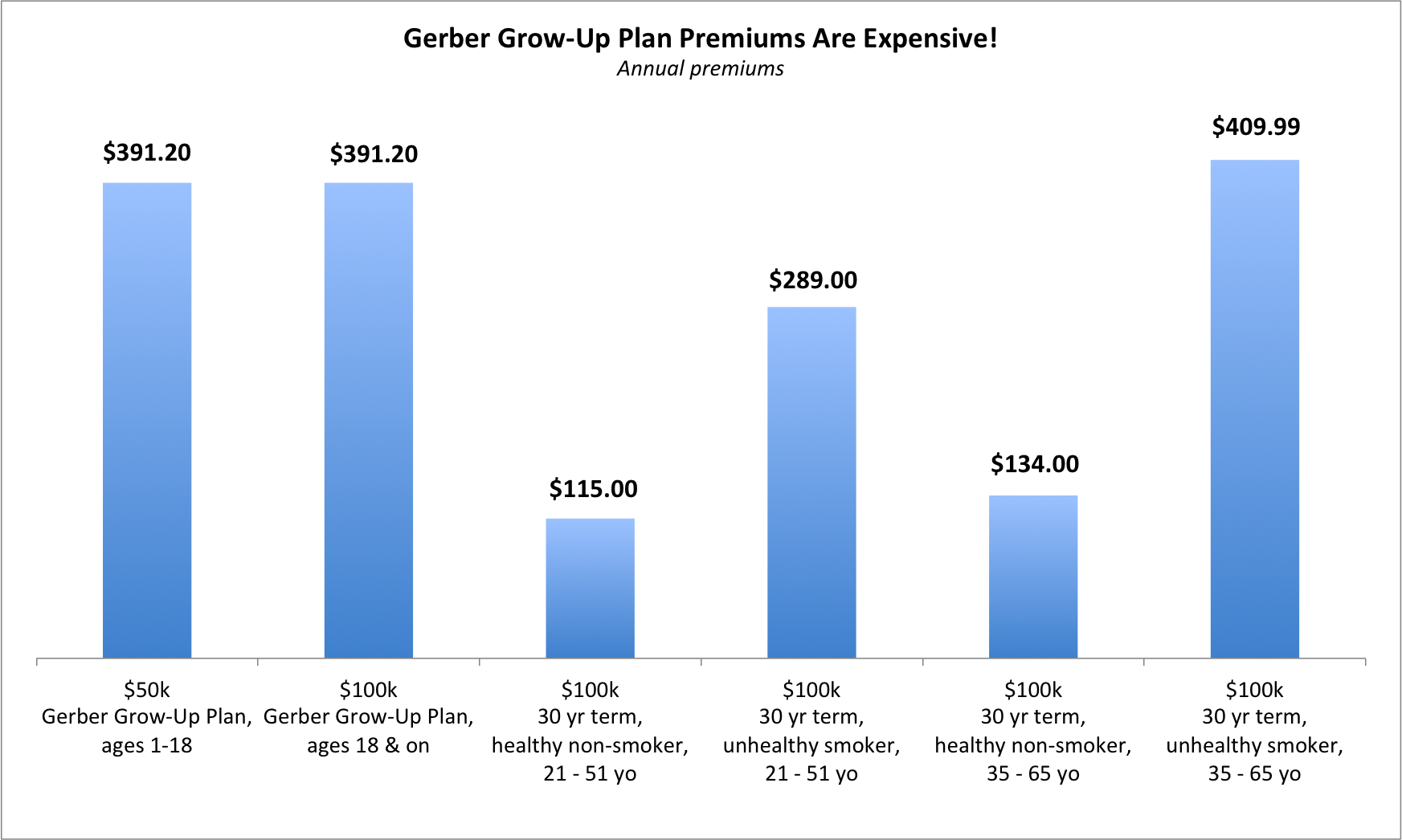

Gerber advertised “$32.60 / month” for my daughter’s $50,000 policy. That’s $391.20 / year. How does $391.20 / year compare to other insurance options?

Not well:

If my daughter waited until age 35 to buy life insurance and were a smoker who's considered less healthy relative to other smokers, we'd still be better off - financially - with 30 year term instead of the Gerber Grow-Up Plan.

Even though it looks like she might “save” nearly $20 / year with Gerber ($409.99 vs. Gerber's $391.20), remember that we'd have paid $13,300 for this "privilege"! ($13,300 = 34 years of $391.20 / year) Definitely not worth it!

If my daughter grows up to be a healthy non-smoker at age 35, or simply chooses to get insurance at age 21, we'd save heaps of money compared to the Gerber Grow-Up Plan.

You might rightly point out that this is term insurance compared to whole life…but the truth is, almost no one needs permanent life insurance. And we already saw in #1 & #2 that Gerber Grow-Up is a bad investment, so why lock your child into paying extra for a bad investment product?

There are some people who will pay rates worse than what’s illustrated here – people with certain rated policies. But we saw in #2 how you could grow your savings in other ways…and stand ready to help your child cover the cost of more expensive insurance on the small chance that’s actually in their future. The far more likely outcome is that your child will have much better ways to get life insurance than with Gerber.

Keep in mind that the pricing above from Gerber only applies to the initial child coverage amount, which doubles at age 18. If your child wishes to increase coverage later on, it will cost even more.

4) Gerber makes it very difficult to get additional insurance

Gerber says: “Your child can purchase up to 10x the original amount of protection!”

The truth is: only a bit at a time, it’s very difficult to get the timing right, and it’s unlikely to be anywhere close to the life insurance coverage the child will one day need

Gerber makes it very difficult to get adequate life insurance under the Grow-Up policy in a reasonable timeframe with a series of read-the-fine-print hoops your child will have to jump through. The whole thing reads like a “gotcha!” scheme.

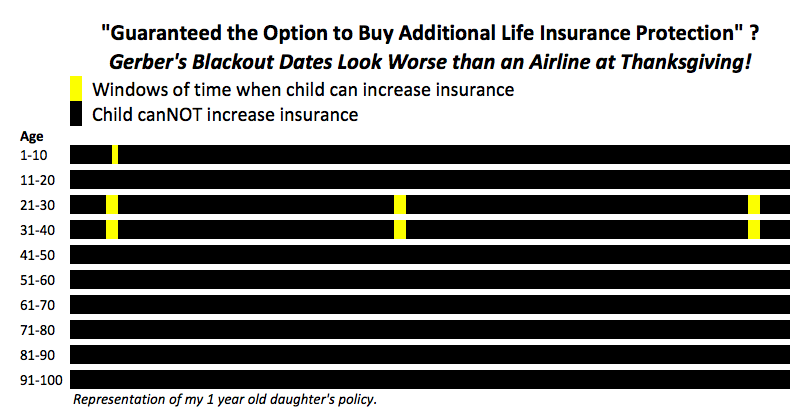

Here's a picture that represents my 1 year old daughter's policy's "Guaranteed Purchase Option Rider" -- that's the technical name for the part of the policy that lets the child increase coverage later in life, regardless of their own insurability.

This picture show you just how tiny the windows of time are in her life when she would be permitted to increase her guaranteed coverage with Gerber: yellow is when she's allowed to increase her insurance, black is when she cannot:

Wow, talk about restrictive. Worse than an airline's blackout dates around Thanksgiving!

Here are the rules, in plain English: the child may only increase coverage 4 times in their life, and never by more than their grown-up coverage amount (the amount the child has when coverage doubles at 18).

Those 4 increases can only happen at specific times:

· The policy purchase anniversary* when the child is age 21, 25, 30, 35 or 40

*Yes, you read that right…your child will need to keep track of the anniversary dates of when their loved ones purchased insurance! And better be precise: Gerber requires written notice of the desire to increase coverage between 30 days prior to 30 days after such policy purchase anniversary date. Sheesh, talk about making it difficult!

· Your child may use one of their permitted age-based increases early if they provide proof to Gerber that they got married or had a child within the last 90 days…oh, and that they hadn’t increased life insurance with Gerber in the prior 9 months either!

Gerber highlights how a $10,000 child policy can become $100,000 in its marketing videos, but they don’t tell you about all the fine-print rules.

Let's imagine how that might actually work. At age 18, the $10,000 coverage doubles to $20,000 (let's call that "the adult coverage amount").

The idea that a 21 or 25 year old will be excited to cut a check each month for increased permanent life insurance seems a little...unrealistic.

If the child misses a window, they can't get it back.

If the now-grown child becomes a parent sometime age 26-30, they can use the age 30 increase early but only if they remember to notify Gerber and request an increase 90 days after having the child...all while in the exhausted haze that is the first 3 months of new parenthood.

But each increase is limited to the adult coverage amount ($20,000 in this example.) So now the child is a parent themselves, with only $40,000 insurance, and they've “used up” their age 30 increase.

Let’s imagine a younger sibling arrives when the grown child is age 31…let’s again assume that proper notice within 90 days is given…now they have $60,000 insurance…they cannot recoup prior unused insurance increases, and they’ve already used up their age 35 increase early.

If the adult child (now a parent of two) wants more than $60,000 guaranteed coverage insurance with Gerber, they’ll have to wait until age 40, and be sure to hit that “plus or minus 30 days from insurance anniversary purchase” window. Even then, they'll only have $80,000 of coverage, hardly enough.

Good Lord, look at how tedious this is, all to get what’s way less insurance than the adult child would ever need!

5) Gerber is very, very expensive life insurance (Part II)

You might wonder: what is the price of future coverage? A lot more than the already-steep premiums for the initial coverage.

If you or the child want to purchase additional insurance in the future, it will not be at that same rate, but rather then-standard insurance rates.

The bill will be big, even at the earliest window for an increase: today, the rate for a 21 year old female in New York is $744 / year for $100k coverage, so my daughter would pay nearly double for her first next $100k of insurance, leaving her with a total bill of $1,135.20 / year for $200k life insurance at age 21.

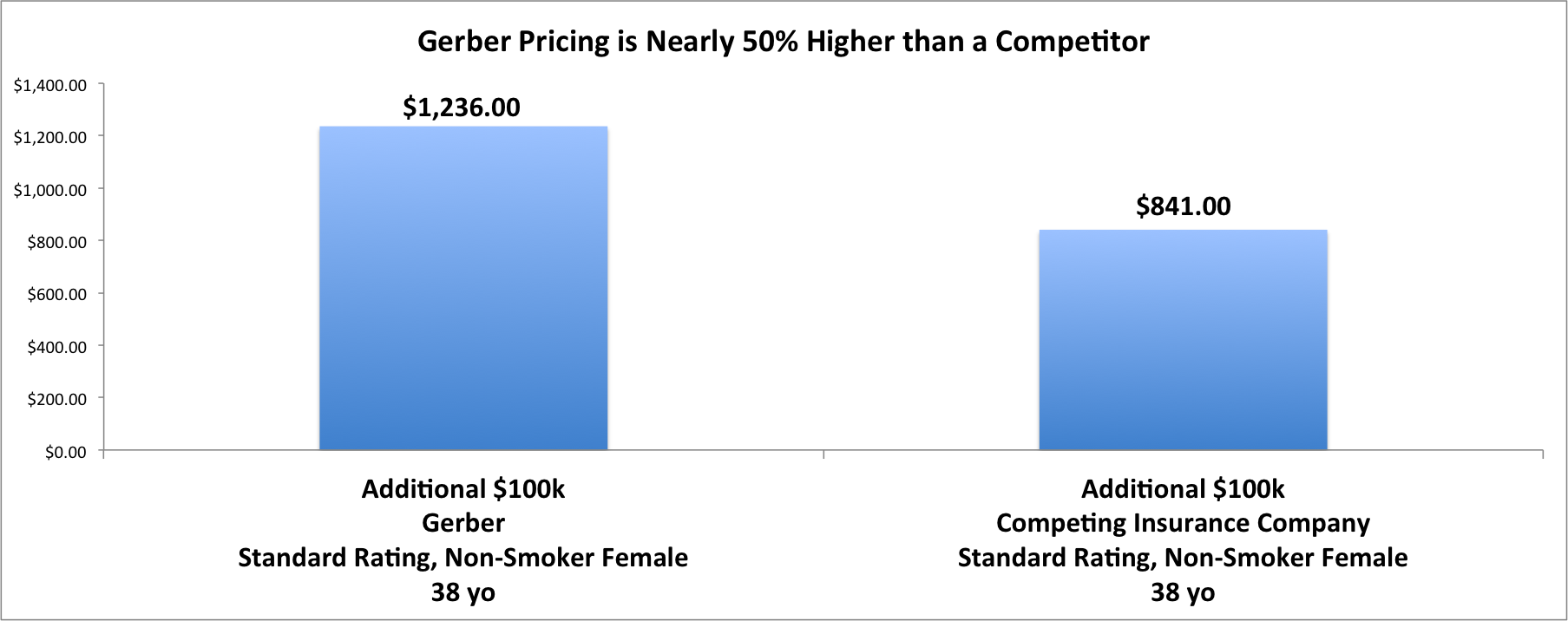

Additionally, Gerber doesn't appear to offer good pricing on permanent life insurance -- I looked into what it would cost to get a permanent life insurance policy for myself IF I received a standard rating.

Keep in mind that a "standard" rating leaves room for significant health issues. "Standard" is typically 4th best pricing and, for some insurance companies, is even available to people who have experienced significant health events, including cancer (though, to be clear, qualifying for Standard would likely require having been in remission / cancer-free for at least 4-5 years). Still, a "standard" rating by no means equates to a sparkling health record with no medical issues!

Gerber's pricing looks expensive vs. other insurance companies for the same product, and same health rating:

Gerber’s rates are nearly 50% above a competing insurance company, for the same rating (standard) for the same product ($100k permanent life insurance).

Why lock in non-competitive rates for an expensive product that most people don’t even need?

Conclusion

I find the Gerber Life Insurance videos heart-breaking – so many parents and grandparents wanting to give their beloved little ones a head start, and seemingly being misled into believing that the Gerber Grow-Up Plan is a good way to achieve that noble goal.

One mom describes with obvious pride:

“It was my mommy moment! I was doing something for my kids!”

Doing everything we can is indeed a hallmark of parenthood. And it’s sad when a company exploits those excellent instincts with a terrible, difficult-to-understand, rip-off product.

Please do not feel badly if you've purchased a Gerber Grow-Up policy - the marketing is excellent and the disclosures are poor. Additionally, I personally experienced customer service so misleading - and in some cases, deceitful - that I was shocked. (That'll be the topic of another post.)

Want to do something that actually gives your little ones a head start?

Make sure that your income - or care you provide for free - are properly insured. It is really tough for kids who lose a parent while they still depend on that parent for financial support and care. Make sure that if tragedy struck, your loved ones would be on sound footing financially. Get a life insurance quote.